Issue 24# - Structuring 2.0 – Smurfing in the Digital Age

Polar Insider | Issue #24 | Week of 13 August 2025

🧊 Introduction

Hi there,

Welcome to this week’s edition of Polar Insider. This time, we’re focusing on a troubling trend in financial crime - how money launderers are evolving traditional structuring techniques, also known as “smurfing,” in the digital age. From exploiting fintech platforms to using artificial intelligence for creating synthetic identities, criminals are finding new ways to evade detection.

Here’s what you’ll find inside this issue:

📌 Top Story – Structuring 2.0 – Smurfing in the Digital Age

🔎 Case Study – How Cross-Border Smurfing Rings Are Exploited

🌍 Regulatory Roundup – Smurfing-Related AML Updates You Need to Know

🧰 Compliance Toolkit – Resources for Detecting Modern Structuring

📌 Top Story

Structuring 2.0 – Smurfing in the Digital Age

Financial activity has gone digital, and so has crime. Money launderers are adapting the traditional technique of breaking up large sums into smaller transactions - known as structuring or “smurfing”- to bypass reporting thresholds. They are now leveraging fintech platforms, crypto transactions, and even AI to stay ahead of compliance controls.

What’s Happening

Structuring has evolved with the advent of digital payments, Buy Now Pay Later (BNPL) services, and AI innovations. Criminals exploit the speed and convenience these platforms offer while concealing their financial footprints. Here are some key developments reshaping the landscape of smurfing:

Digital Payments & Challenger Banks

Platforms offering rapid transactions and easy account setups, such as fintech apps and neobanks, provide an attractive avenue for launderers. These platforms’ lighter AML controls often lead to vulnerabilities. For example, the UK’s Starling Bank faced fines of £28.9 million for failing to detect suspicious small deposits used in structuring schemes.

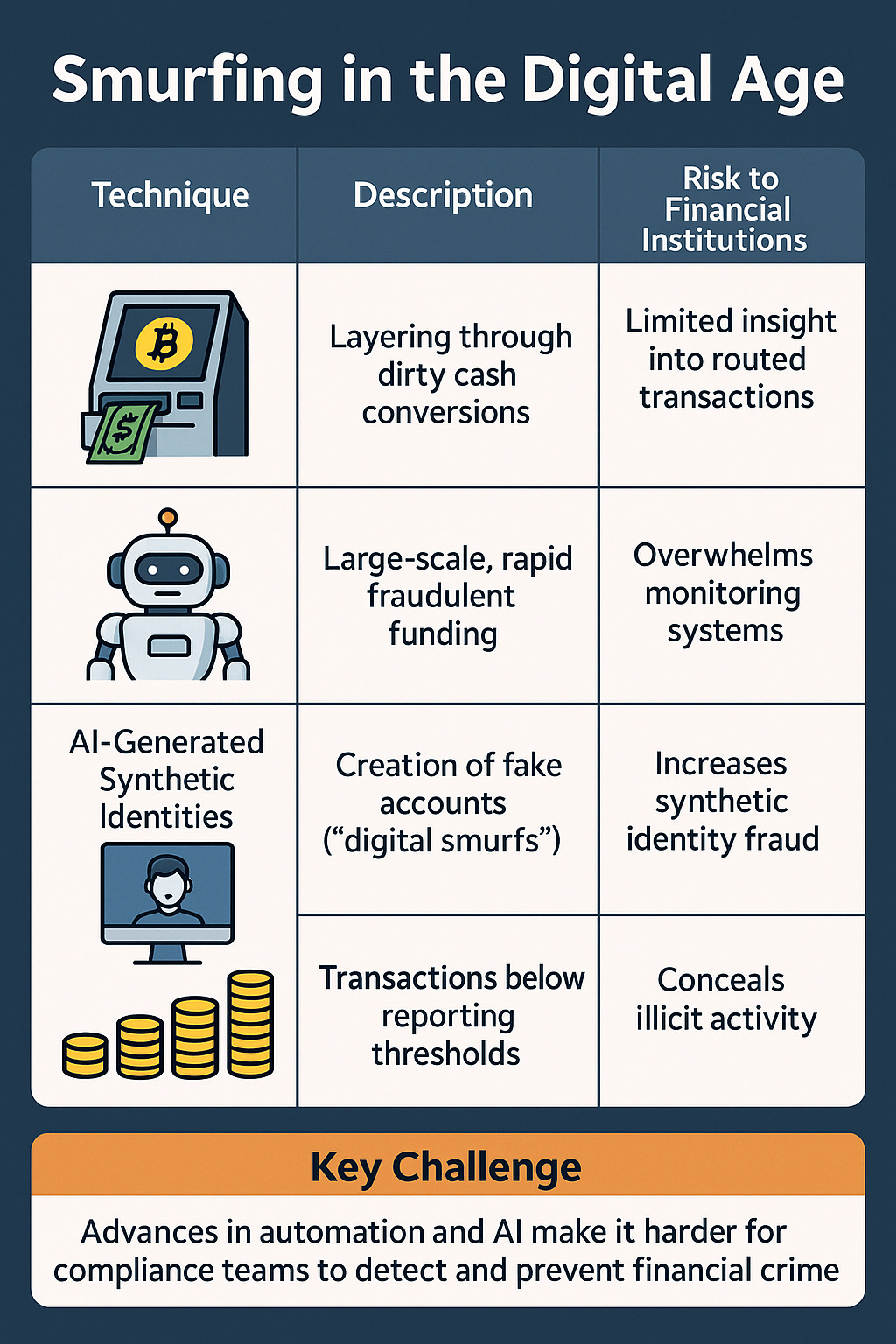

Cryptocurrency & Automation

Cryptocurrency allows criminals to break down illicit funds into crypto wallets in small increments, often using ATMs to convert dirty cash into digital assets. Automation tools, such as bots, enable seamless layering and rapid scaling of funds while evading manual detection.

AI and Synthetic Identities

Generative AI has birthed “digital smurfs”–synthetic accounts created with fake credentials. These fake personas allow criminals to open multiple bank accounts undetected, fragmenting transactions to stay below reporting thresholds.

The Risk to Financial Institutions

Financial institutions face heightened exposure due to these advancements in structuring techniques. Key risks include lost visibility over transactions routed through intermediaries, high volumes of micro-transactions designed to evade detection, and fraud enabled by synthetic identities. Furthermore, institutions that fail to act face regulatory scrutiny and crippling penalties.

What You Can Do

Here are four actionable strategies that compliance teams can adopt to counter this evolving threat:

✅ Invest in AI-Powered Analytics

Use machine learning to recognize atypical patterns in transaction data. AI tools can detect nuanced structuring “fingerprints,” such as timing anomalies, dispersed networks, or clusters of linked accounts.

✅ Implement Cross-Channel Monitoring

Consolidate transaction data across all channels, ensuring your systems detect when criminals mix cash, crypto, and fintech platforms. A unified view helps connect the dots across multiple accounts and platforms.

✅ Deploy a Risk-Based Approach to AML

Tailor monitoring and thresholds based on customer risk levels. High-risk customers like cash-intensive businesses should trigger enhanced due diligence and monitoring.

✅ Prioritize Staff Training

Empower employees with training on emerging structuring typologies. For example, teach tellers to recognize red flags, like repeated deposits under reporting limits.

🧠 Pro Tip: Regularly test your monitoring systems with simulated structuring patterns to ensure detection mechanisms remain effective.

🔎 Case Study

Cross-Border “Smurfing” Ring Busted in Florida

Location

Orlando & Miami, Florida

Enforcement Agencies Involved

Internal Revenue Service – Criminal Investigation (IRS-CI)

Federal Bureau of Investigation (FBI)

U.S. Attorney’s Office for the Middle District of Florida

U.S. Department of Justice (DOJ)

What Happened

A 2024 investigation uncovered a sophisticated laundering enterprise based in Florida, centering on fake businesses designed to funnel proceeds from Business Email Compromise (BEC) schemes. Led by Cristian R. Labour and four associates, the group set up entities such as L&A Products Distribution Inc., Appliances Electronics & More LLC, Advanced Technologies & Computers LLC, and USA Home Goods Distribution Inc.

They used these businesses to receive fraudulent wire transfers from BEC victims who believed they were paying legitimate vendors, only to have their payments rerouted to accounts controlled by the defendants.

Execution

The group laundered more than $1.8 million using a two-pronged strategy:

Immediately wiring the majority of the funds to China under the guise of legitimate payments for goods.

Withdrawing a share in cash through structured transactions—always keeping each transaction under $10,000 to avoid triggering Currency Transaction Reports (CTRs).

For example, in just over two weeks in March 2021, two operatives funneled over $560,000 into a single account, wired out more than $400,000 abroad, and withdrew roughly $80,000 in small increments via various ATMs and bank branches.

Charges Filed (2024)

Conspiracy to commit money laundering

Multiple counts of money laundering and structuring financial transactions

Identity theft and use of false documents

Outcome

Cristian R. Labour and several associates ultimately pleaded guilty. The U.S. Department of Justice underscored this prosecution as a prime example of structuring entwined with international laundering schemes. Law enforcement highlighted the crucial role of financial institutions' Suspicious Activity Reports (SARs) and strong inter-agency coordination in dismantling the criminal network.

Discovery & Aftermath

Investigators linked suspicious activity across multiple accounts, spotting red flags such as frequent incoming wires followed by immediate outbound international payments. Compliance teams and law enforcement worked together to connect the web of accounts and movements, leading to federal indictments of those involved.

Key Lessons for Financial Crime Teams

🚨 Improved Business Verification

Ensure comprehensive Know Your Customer (KYC) checks for new accounts, especially those claiming to operate cash-intensive businesses or industries associated with higher laundering risks.

🔐 Fine-Tuned Monitoring Systems

Adjust monitoring rules to detect unusual sequences, such as incoming wires swiftly followed by structured withdrawals or foreign transfers.

🧱 Collaborative Intelligence Sharing

Pool insights across departments or institutions to detect broader patterns of linked account activity. Cross-border data-sharing agreements can amplify these efforts.

🌍 Regulatory Roundup

🇺🇸 North America

· Lowering Reporting Thresholds: The U.S. has introduced geographic targeting measures requiring firms in high-risk areas to report cash transactions exceeding $200. This targets structuring hotspots linked to cartel operations.

· Focus on Crypto ATMs: FinCEN flagged cryptocurrency kiosks as a growing avenue for smurfing, advising tighter oversight and reporting requirements.

🇪🇺 Europe

· Harmonized Cash Limits: The EU introduced a continent-wide cap of €10,000 on cash transactions. New limits are expected to close gaps for structuring while imposing stricter oversight on large commercial payments.

🇦🇺 Asia-Pacific:

· BNPL Regulation: Australia now mandates AML programs for BNPL providers, aligning their oversight with other financial institutions. E-money platforms and wallets are also under increased scrutiny.

Key Message

Global regulatory landscapes are tightening. Financial institutions must stay proactive by updating compliance policies, especially for tech-based payment platforms, to align with these changes.

🧰 Compliance Toolkit

Equip yourself with these resources to tackle structuring risks effectively:

• AUSTRAC Guide – Cuckoo Smurfing Typology

📎 Link → Detect and report cuckoo smurfing | AUSTRAC

• FinCEN Notice – Crypto ATMs and Structuring Red Flags

Link → Alerts/Advisories/Notices/Bulletins/Fact Sheets | FinCEN.gov

• FinCEN Alert – Deepfakes and Funnel Accounts

📎 Link → https://www.fincen.gov/sites/default/files/shared/FinCEN-Alert-DeepFakes-Alert508FINAL.pdf

💬 Quote of the Week

“Breaking transactions into small pieces will not stop us from seeing the bigger picture."

IRS Criminal Investigation Division

🎁 Bonus for Subscribers

Don’t forget to download your copy of the 2025 Financial Crime Regulatory Tracker (USA, UK, AU).

Stay on top of AML requirements and enforcement trends globally.